It’s been a good week for extremes in the housing market with rates at 3 month lows, pending home sales at “record” lows, and conforming loan limits up to record highs. Here’s why at least two of those three things aren’t very interesting.

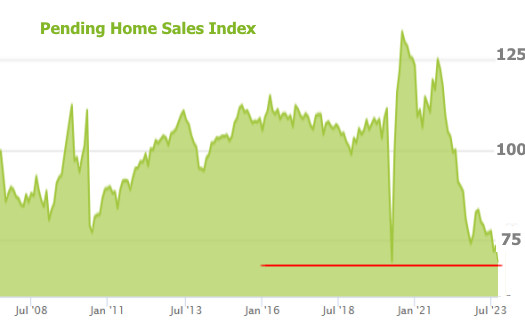

Let’s start with what was probably the week’s most dramatic housing market headline: record low pending home sales. Sounds scary, no?

By no means should we think that the housing market doesn’t have a care in the world. To be sure, existing homes (and by extension, Pending Home Sales) have suffered on a combination of higher rates and lower inventory, but there are several counterpoints to historically low sales numbers.

The “record” low reported by the National Association of Realtors this week is actually slightly higher than the number initially reported (and subsequently revised) in May 2020. More importantly, it just wasn’t very far from last month’s reading, nor was it a departure from the prevailing trend.

Simply put, pending sales had been in a high, stable trend before covid. Demand surged early in the pandemic when rates and prices were lower. Sales dried up quickly as prices and rates soared, AND as fewer sellers were willing to list their homes for sale.

This is in stark contrast from the low sales counts surrounding the Great Financial Crisis which saw abundant inventory, lower prices, and lower rates. In other words, it makes sense for home sales to be in the toilet, and it will make sense to see them climb out once rates improve more meaningfully.

Conforming Loan Limits

This week also brought the release of home price data from the US government. When Q3 data comes out in late November, it results in an update to the conforming loan limit (CLL), which will always be higher as long as home prices are higher than they were a year ago.

But what does the CLL even mean? It’s not a big dramatic thing and it is only really newsworthy for buyers who needed a loan that was just a bit larger than the previous loan limit.

The CLL is the maximum amount that Fannie Mae and Freddie Mac will guarantee as a conforming loan. Conforming loans have a uniform set of underwriting guidelines and pricing adjustments that tends to result in a streamlined approval process and lower rates compared to other mortgage options.

This year, the CLL increased from $726,200 to $766,550, a reflection of the 5.5% year-over-year increase in home prices measured by the Federal Housing Finance Agency (FHFA). There are higher loan limits for certain counties and property types. More info is available here.

Rates at 3 Month Lows

Now we’re getting into things that are more interesting, at least if we’re looking at rates in a more recent context.

If we zoom out to a longer-term context, this is only the beginning of what some analysts think will be the last big reversal that we’ll see for a while in the rising rate trend of the past few years.

We’re careful to qualify the rate reversal as a thing that “some analysts” expect as opposed to a sure thing. Sure things are incredibly rare when it comes to the future movement in interest rates and even then, they tend to only exist as conditional generalities.

Whether or not the current potential bounce proves to be THE bounce we’re looking for is HIGHLY conditionally dependent on upcoming economic data. In not so many words, the economy has reached a point where it’s starting to show signs that the Fed’s rate hikes have cooled inflation and growth off enough that the Fed could soon have the opportunity to consider cutting rates.

“Soon” in this context is measured not in days or weeks, but months–2 or 3 of them at least. It would also not happen all at once, but instead be a gradual process informed by key economic reports along the way.

With that in mind, the upcoming week brings several key economic reports with Friday’s Jobs Report being the most important. If the data is weaker than economists’ forecasts, rates would likely move lower. If the data is stronger–especially if it’s much stronger–the market’s dialogue will quickly shift from the potential for early 2024 Fed rate cuts to the possibility of additional rate HIKES.

To reiterate, big increases or decreases in rates are highly conditionally dependent on economic data. The more cohesive the message in the data and the stronger the message (i.e. every single report next week coming in much better or much worse than forecast) the bigger the potential reaction in rates.

Even then, with an important Fed announcement coming up the following week, some of the potential reaction to next week’s data will be on hold until traders see what the Fed has to say.