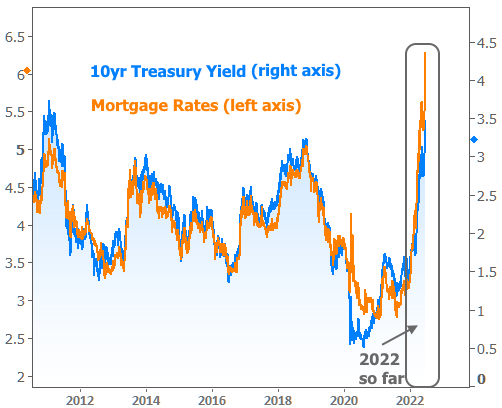

In a year where mortgage rate volatility has been extreme, this week made everything else look tame by comparison. While it will never show up in weekly survey numbers, the 3-day jump between last Thursday and this Tuesday was one of the biggest on record, taking the average 30yr fixed quote from 5.55% to 6.28% by yesterday afternoon. The pace of that spike is nothing short of staggering considering 5.55% was already near their highest levels in more than a decade.

The drama began with last Friday’s Consumer Price Index (CPI), a key inflation report that showed prices rising faster than expected. Inflation is biggest concern for the Fed at the moment, and the biggest reason for their increasingly aggressive efforts to push rates higher in 2022.

CPI alone wouldn’t have been worth this much drama were it not for the looming Fed announcement on Wednesday afternoon. Further complicating matters was the fact that the Fed refrains from public comment on monetary policy in the 12 days leading up to a policy announcement. In other words, markets were flying blind as to what the Fed’s response might be to the CPI data, and imaginations ran wild.

The best guess was that instead of hiking rates by 0.50%, the Fed would instead opt for 0.75%. Indeed they did, and shortly thereafter, mortgage rates began to fall.

FALL?! How can that be?! If the Fed hiked 75bps, wouldn’t mortgage rates rise by 75bps?

This question speaks to a popular misconception about the Fed and mortgage rates. In short, when the Fed hikes rates, it does NOT mean that mortgage rates go higher (except for the small contingent of loans that are actually tied to an index that moves with the Fed Funds Rate). In fact, it frequently means that rates move lower.

Why would a rate hike lead to lower rates?

The short answer is that the bond market (which dictates mortgage rates) has almost always already adjusted for the rate hike ahead of time. By the time the Fed actually hikes, it’s old news to the market, and there’s a sense of relief as traders have one less uncertainty to deal with.

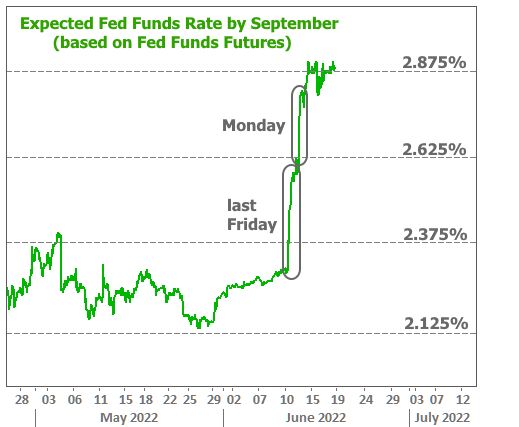

The following chart shows these rate hike expectations in action. Fed Funds Futures allow traders to bet on expected Fed rate levels in the future. Here’s how the futures contracts were trading for this week’s meeting:

Notice the fairly small reaction on Friday relative to the follow-through seen on Monday. Some of this has to do with momentum and the evolving thought process of traders as they consider the implications of data. But if we look at Fed Funds Futures for September, we can see the market was already added more than a quarter of a percent to its Fed rate expectations, just a bit farther into the future.

In other words, the market instantly knew Friday’s inflation data meant more than another quarter point in rate hikes. Then on Monday, the market decided it was worth another quarter point on top of that. Incidentally, the increase in longer term Fed rate expectations though Tuesday (0.63%) was very similar to the increase in mortgage rates (0.71%).

All that to say that by the time the Fed finally pulled the trigger on its 0.75% rate hike, it was old news to the bond market. This explains why rates didn’t go any higher after the Fed Announcement, but it doesn’t explain why they fell. For that, we needed the help of Fed Chair Powell during the post-announcement press conference.

What did Powell say? The most important comment was that 0.75% rate hikes will not be common. That’s all it took to send the bond market surging toward the best levels of the week. Despite significant volatility from moment to moment, a generally stronger trend remained intact through the end of the week. After being as high as 6.28% on Tuesday, 30yr fixed rates were down to 6.03% by Friday mid-day.

So should we lament the jump up into the 6% range for the first time since 2008? Sure, feel free! No one likes high rates. Even if our venerable elders and students of history are quick to remind us about rates being much higher in the 80s, this move has been painful. Home’s also cost quite a bit more relative to incomes today, but we’re not looking to pick any fights with baby boomers.

Once you’re done lamenting and arguing with the finance scholars at the bingo parlor, feel free to breathe a sigh of relief. Why? Because this is finally the magnitude of upward momentum we’ve been talking about for months and months–the kind that’s required to more completely price in the reality of the Fed rate hike outlook–the kind that has quite clearly helped pump the brakes on a majority of exuberant real estate markets.

Are we saying to rest easy while rates plummet and housing heals? Not hardly! We’re saying that this is when the healing can begin… maybe. Rates are finally high enough that we can legitimately assess the next long-term ceiling.

A word of warning though: that ceiling can only be confirmed by economic data–specifically: inflation data. Inflation has to fall back to more normal levels before anyone can rest easy that rates will follow. The point is that rates (especially mortgage rates) have now done quite a bit to react to the shift in Fed policy at the beginning of the year–traversing more than a decade’s worth ups and downs in a few short months.

As for Treasuries, yields are now high enough as to be pricing in virtually all of the expected Fed rate hikes over the next year. Once that happens, the only way for them to go much higher is for the data to deteriorate further. Bottom line: if we can avoid upside inflation surprises like last Friday’s, we may have just seen the highest rates of the year.